“Salary aayi toh sapne Amazon cart mein dhal gaye,

Gen-Z ke armaan ab EMI ke instalments mein pal gaye.

Har swipe pe khushiyon ka screenshot toh milta hai,

Par sukoon… ‘Pay Later’ ke interest mein kahin kal gaye.”

India is witnessing a profound transformation in its financial and cultural landscape. Once defined by a cautious savings-oriented mindset, modern urban India increasingly thrives on credit-driven consumption. Equated Monthly Instalments (EMIs), originally designed as tools for economic accessibility, have evolved into instruments sustaining aspirational lifestyles. From smartphones and luxury vacations to weddings and online shopping, almost every aspect of modern consumption can now be purchased through deferred payment systems. This article examines the emergence of what may be called “India’s Pay-Later Generation” — a generation earning more than previous ones, yet simultaneously experiencing rising financial anxiety and emotional exhaustion. The rise of social media, digital lending platforms, fintech revolutions, and Buy-Now-Pay-Later systems has normalised debt as a lifestyle rather than an emergency measure. In this environment, ownership appears immediate, but repayment becomes permanent.

The essay further explores how consumer culture has shifted the psychology of spending. Modern consumers no longer ask whether they can truly afford something; instead, they evaluate whether they can manage the monthly instalment. This subtle psychological transition has transformed financial behaviour across India’s growing middle class. Beyond economics, the article investigates the emotional consequences of instalment culture: stress, burnout, performative prosperity, fear of instability, and declining financial freedom. While EMIs undeniably enable mobility, education, and access to opportunities, unchecked consumerism risks creating a society trapped between aspiration and indebtedness. Ultimately, this article argues that India’s modern financial crisis is not merely about money, but about identity, visibility, and the growing confusion between luxury and happiness. In a culture obsessed with instant gratification, the greatest casualty may quietly be peace itself.

The Steel Box and the Push Notification

For generations, the bedrock of the Indian household economy was anchored in a tangible, unyielding philosophy of financial restraint. This ethos was physically manifested in the ubiquity of the rusted steel box, the hidden folds of kitchen spice jars, and the meticulously maintained postal savings passbooks. To the traditional Indian household, money was a scarce resource requiring protection, and spending was an act of deliberate necessity. Financial health was measured strictly by the depth of one's reserves. Debt (karza) was viewed not as a tool for leverage, but as a profound moral and social burden—a state of vulnerability to be avoided at all costs, spoken of in hushed, cautionary tones.

In the span of less than two decades, this century-old psychological fortress has undergone an unprecedented systemic collapse. The contemporary urban landscape is no longer defined by the quiet accumulation of physical currency, but by the relentless chime of digital notifications. Across India's major metropolitan areas and tier-2 cities, a new generation of consumers wakes up to automated warnings that whisper a singular, recurring phrase: “Your EMI is due tomorrow.”

This transition marks a profound evolutionary leap from a cash-surplus, high-savings mindset to an ecosystem built on continuous, leveraged consumption. The macroeconomic numbers validate this shift. India's household debt surged to 41.3% of Gross Domestic Product (GDP) by the end of March 2025, a stark escalation from its historical five-year average of 38.3%. This rapid rise in the household debt-to-GDP ratio has introduced distinct vulnerabilities into the domestic economy, with consumption-related loans accounting for the vast majority of these borrowings.

The fundamental paradox of this generation is stark: they are earning more than any of their predecessors, yet they possess significantly less psychological peace. The contemporary young professional commands disposable income that would have seemed impossible a generation ago. However, this wealth is highly fragmented. Because e-commerce platforms, automotive brands, and luxury services have decoupled the joy of acquisition from the immediate pain of payment, the modern Indian consumer evaluates affordability through a distorted lens. They no longer ask, “Do I have the money to buy this object?” Instead, they ask, “Do I have enough room in my monthly cash flow to absorb this instalment?”

This subtle cognitive shift has fundamentally redefined the concept of ownership. Dreams—whether an international vacation, a premium smartphone, or a designer wedding—arrive instantly. But the psychological cost of these aspirations is drawn out across months and years. In this hyper-financialised lifestyle, the sense of immediate ownership is an illusion; the true constant is the permanent state of repayment.

The Great Epistemological Shift: Redefining Affordability

To understand the mechanics of India's "Pay-Later Generation," one must examine the psychological restructuring of the consumer mind. Historically, the purchase of an asset required an arduous process of delayed gratification. Saving was an active, prolonged ritual that reinforced the value of the target acquisition. The "pain of payment"—a well-documented cognitive friction in behavioural economics—acted as a natural psychological barrier against impulsive expenditures (Deepika & Meena, 2025; Nair, 2026). When a consumer had to count out physical banknotes to purchase a television, the physical reduction of their cash reserves directly activated the brain's insular cortex, generating an aversion response that limited reckless spending.

The rise of the Equated Monthly Instalment (EMI) and its contemporary evolution, the Buy-Now-Pay-Later (BNPL) model, has systematically eliminated this cognitive friction. By dissolving a high lump-sum cost into small, ostensibly harmless monthly fragments, financial technology has engineered a highly effective cognitive bypass.

From Absolute Value to Fragmented Cash Flows

When a premium consumer product costing ₹80,000 is presented as a singular price tag, the rational mind evaluates it against total current net worth and near-term security. However, when that same product is presented as a "No-Cost EMI" of ₹6,666 per month over twelve months, the asset is stripped of its absolute economic weight. The consumer does not view the transaction as an ₹80,000 reduction in lifetime wealth; they view it as a manageable operational expense against their upcoming paycheck.

This transformation has completely remapped how the expanding middle class evaluates their purchasing power:

- The Deconstruction of Affordability: Affordability is no longer treated as a static equation of capital reserves vs. asset cost. It has been transformed into a dynamic, precarious assessment of future cash-flow capacity. The modern consumer confidently operates under the assumption that their future earning potential is completely secure, predictable, and upwardly mobile.

- The Erasure of the "Pain of Payment": The frictionless design of digital lending applications deliberately detaches the pleasure of immediate consumption from the future pain of financial drainage (Deepika & Meena, 2025; Nair, 2026). Because the transaction requires only a biometric scan or a single-tap authorisation, the cognitive warning systems that once protected household wealth are completely neutralised.

- The Mirage of "Zero Cost": The widespread marketing of "No-Cost EMIs" serves as a highly effective psychological mechanism. By absorbing the interest component within merchant discounts or processing fees, financial institutions remove the guilt of borrowing. The consumer believes they are outsmarting the system by utilising interest-free leverage, overlooking the reality that they are locking themselves into a long-term cycle of mandatory cash outflows.

This psychological renegotiation has cleared the path for credit to transform from an emergency safety net into a core component of daily lifestyle architecture.

The Digital Architecture of Entrapment

The shift toward a leveraged lifestyle is not merely a spontaneous cultural trend; it is an engineered phenomenon powered by an aggressive, highly sophisticated financial technology infrastructure. The convergence of India's unified public digital infrastructure—such as the Unified Payments Interface (UPI) and India Stack—with venture-capital-funded fintech algorithms has created an incredibly frictionless borrowing environment in global financial history.

The Fintech Assembly Line

A decade ago, securing a consumer loan required physical documentation, salary slips, bank branch visits, and days of underwriting scrutiny. This procedural drag functioned as a protective structural barrier, deterring all but the most determined borrowers. Today, that entire infrastructure has been replaced by a lightning-fast, data-driven digital assembly line.

By leveraging alternative data sources—including e-commerce purchase histories, ride-hailing app patterns, food delivery frequencies, and smartphone SMS histories—fintech algorithms can generate a comprehensive credit risk assessment within milliseconds. The result is a total lack of friction. A consumer browsing an e-commerce catalogue at midnight can be targeted with a pre-approved, customised BNPL line of credit at the exact moment of peak emotional desire.

The Dynamics of BNPL vs. Traditional Credit Cards

While traditional credit cards require a formalised application process and are typically reserved for individuals with established credit histories, Buy-Now-Pay-Later (BNPL) platforms have successfully democratized debt down to the youngest and lowest-income segments of the population (Kumar et al., 2024).

| Features | Traditional Credit Cards | Buy-Now-Pay-Later (BNPL) Platforms |

Target Demographic | Salaried individuals, established corporate workers, and mature credit profiles. | Gen Z, college students, first-time job seekers, gig-economy workers (Kumar et al., 2024). |

Underwriting Friction | Stringent credit bureau verification, mandatory CIBIL score checks, and salary verification. | Soft credit checks, alternative data footprinting, instant algorithmic underwriting (Mojon, 2023). |

Transaction Focus | High-value assets, institutional purchases, recurring premium billing. | Low-ticket items, everyday clothing, food deliveries, and minor lifestyle luxuries (Kumar et al., 2024). |

Credit Bureau Integration | Mandatory, immediate reporting of all balances, utilizations, and delays. | Often fragmented or unreported for minor amounts, masking aggregate consumer leverage (Mojon, 2023). |

Average Order Size Impact | Moderate increase based on established, rigid credit limits. | Drives an empirical increase of roughly 6.42% in total online order size (Kumar et al., 2024). |

The Mechanics of Algorithmic Micro-Targeting

Fintech platforms no longer wait for consumers to seek out credit; they proactively embed credit solutions directly into the software interfaces of daily life. Machine learning models continuously track user behaviour. If an individual adds an item to an online cart and hesitates at the payment page for more than thirty seconds, the system dynamically alters the interface to display a customised, fragmented payment option.

These micro-loans are packaged in friendly, lifestyle-focused language. Terms like loan, interest, principal, and collateral are intentionally replaced by softer concepts like pocket money, pay later, split-it, and slice. This calculated linguistic shift detaches micro-borrowing from its heavy historical associations with financial distress, rebranding it as a modern tool for smart personal optimisation.

Performative Prosperity and Social Media Overdrive

The institutional availability of credit would not be nearly as potent if it were not accelerated by a powerful cultural force: the rise of a hyper-visual digital social space. The explosion of platforms like Instagram, YouTube, and LinkedIn has established a cultural regime of performative prosperity. In this ecosystem, social standing, personal success, and human value are directly tied to the public exhibition of curated luxury.

The Democratisation of the Luxury Aesthetic

Historically, elite luxury was naturally protected by its prohibitively high cost; it belonged exclusively to those who had accumulated substantial wealth over decades. Today, the combination of digital access and micro-credit has democratised the luxury aesthetic, decoupling the appearance of wealth from its actual possession.

Hyper-Visual Social Media

(Curated lifestyles & peer envy)

│

▼

Performative Prosperity Focus

(Need to broadcast success instantly)

│

▼

Fintech Micro-Leverage

(Immediate financing of luxuries via EMI)

│

▼

Gilded Entrapment

(Highly visible status, hollowed savings)

A twenty-three-year-old entry-level corporate employee earning a modest salary cannot afford a ₹1,30,000 flagship smartphone, a luxury weekend getaway to a premium resort, or a designer wardrobe through traditional savings. However, when fintech platforms allow them to finance these experiences through overlapping EMIs, the barrier vanishes. The modern consumer can easily construct a digital persona that signals elite wealth, using short-term consumer credit to project an image of long-term economic success.

The Vicious Cycle of Peer Envy

Social media algorithms are explicitly engineered to amplify lifestyle envy. When an individual's feed is filled with peer groups broadcasting international vacations, high-end automotive purchases, and elaborate cafe experiences, a powerful psychological response is triggered:

- Relative Deprivation: The viewer does not compare their financial reality to broader national averages; they compare it directly to the top 1% of their immediate digital social circle.

- The Compressed Timeline of Success: Traditional milestones that once required fifteen years of professional dedication—such as international travel or luxury vehicle ownership—are now demanded within the first twenty-four months of a career.

- The Financialization of Self-Worth: To prevent a sense of social exclusion, the young consumer feels an urgent need to match these consumption patterns immediately. Because their actual savings cannot support this compressed timeline, they rely heavily on micro-leverage to close the gap.

This creates a highly unstable cycle. The consumer uses debt to purchase an experience solely to broadcast it; their peers witness the broadcast and turn to credit to match it. The entire social ecosystem is propelled into a state of competitive consumption, funded not by genuine economic surplus, but by the systemic financialization of future paychecks.

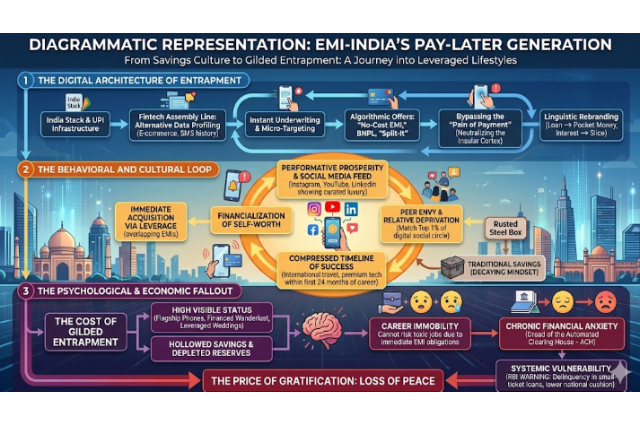

The diagrammatic representation of "EMI-India's Pay-Later Generation."

This visual breaks down the concept into three interconnected cycles:

- The Digital Architecture (Top): Shows how modern tools like UPI, alternative data profiling, and linguistic rebranding (e.g., "Pocket Money" instead of "Loan") make credit instantaneous and remove the typical "pain of payment."

- The Behavioural Loop (Centre): Illustrates how hyper-visual social media and performative prosperity create lifestyle envy, leading to immediate acquisition via leverage (EMIs).

- The Psychological & Economic Fallout (Bottom): Depicts the resulting state of "Gilded Entrapment"—high visible status masking career immobility, financial anxiety, and the rapid depletion of savings, all under the shadow of the RBI's systemic warnings.

Case Studies: The Anatomy of Modern Consumption

To see how these systemic forces play out across the expanding middle class, we can examine three distinct case studies that reflect the realities of contemporary urban India.

Case Study 1: The Premium Smartphone Trap

- Profile: Rohan, a 24-year-old software engineer based in Bengaluru.

- Income: ₹65,000 net monthly salary.

- The Transaction: Driven by peer dynamics at his workplace and the visual culture of his social circle, Rohan purchased a flagship premium smartphone priced at ₹1,20,000.

- The Financial Vector: Instead of waiting until he could save the capital, he chose an 18-month "No-Cost" EMI plan structured at ₹6,666 per month.

- The Economic Fallout: On paper, the commitment seemed entirely manageable, representing roughly 10% of his take-home pay. However, six months into the repayment cycle, Rohan's smartphone encountered accidental screen damage that required an unexpected ₹18,000 repair. To fund this, he had to open a secondary consumer durable loan via a fintech app. When combined with his existing smartphone EMI, his total monthly credit commitment for a single device jumped to over ₹9,000. Rohan found his disposable cash flow heavily restricted, forcing him to rely on credit cards for routine monthly expenses like groceries and utilities.

Case Study 2: The Financed Wanderlust

- Profile: Ananya (27) and Vikram (29), a dual-income corporate couple living in Gurugram.

- Income: Combined monthly take-home of ₹1,80,000.

- The Transaction: Eager to match the travel trends dominating their social feeds, they booked a luxury holiday to Southeast Asia priced at ₹2,500,000.

- The Financial Vector: A digital travel booking platform offered an integrated "Travel Now, Pay Later" feature, allowing them to finance the vacation through an upfront payment of just ₹20,000, with the remaining balance spread across a 24-month personal loan at a 14% annual interest rate.

- The Economic Fallout: While the trip provided an immediate wealth of content for their digital networks, the long-term financial reality was punishing. The monthly repayment stood at ₹11,500. A year into the loan, the couple decided to move to a new apartment to shorten their workplace commute, which required a significant security deposit and upfront relocation costs. Discovering that their savings were completely depleted due to the monthly vacation payments, they were forced to take out an additional short-term personal loan. A holiday that lasted just seven days locked them into an escalating, multi-year web of institutional debt.

Case Study 3: The Leveraged Luxury Wedding

- Profile: Meera, a 28-year-old marketing manager in Mumbai.

- Income: ₹90,000 monthly salary.

- The Transaction: Planning her wedding, Meera faced intense social pressure to deliver a highly photogenic event. The cost for premium venues, designer clothing, and high-end catering quickly escalated to ₹15,000,000—far exceeding her family’s allocated savings.

- The Financial Vector: Meera utilised multiple quick-disbursal personal lending applications to secure ₹6,00,000 across three separate loans, with repayment windows ranging from 36 to 48 months.

- The Economic Fallout: The wedding was a major social media success, but Meera entered her new marriage carrying a combined monthly EMI burden of ₹22,000. When her husband faced a corporate restructuring that resulted in a temporary 20% salary reduction, their household budget collapsed. The rigid, automated nature of her EMIs left zero room for adjustment. The couple had to make extreme lifestyle sacrifices, descending into severe marital friction and anxiety over the fear of defaulting on loans taken out for a single weekend of celebration.

The Deep Socio-Psychological Toll: Gilded Entrapment

The consequences of living a leveraged life extend far beyond simple balance sheet equations; they manifest as a profound transformation in human psychology, emotional resilience, and social behaviour. When an individual’s future labour is completely committed to servicing past consumption, their relationship with work, time, and identity undergoes a damaging shift.

The Psychology of Chronic Financial Stress

Unlike traditional long-term investments like a home loan—which builds equity over time—consumer debt depreciates rapidly. Paying for an asset or experience that has already lost its novelty or utility creates a powerful form of cognitive dissonance. The consumer is forced to sacrifice their current cash flow to pay for a past impulse, turning the monthly EMI payment into an active source of resentment and psychological drain.

These dynamics drive a distinct psychological cycle:

- The Trap of Career Immobility: To take a professional risk—such as exiting a toxic workplace, transitioning to a new industry, or launching an entrepreneurial venture—an individual requires a financial cushion. A young worker whose income is heavily leveraged across four distinct consumer EMIs cannot afford even a single month of income disruption. They are forced to remain in stressful corporate roles out of sheer economic necessity, turning their career into a survival mechanism dedicated entirely to servicing debt.

- The Dread of the Automated Clearing House (ACH): In the modern digital banking framework, repayments are driven by automated debits directly from bank accounts on specific days of the month. The arrival of the first week of the month changes from a time of reward into a period of acute anxiety. The automated nature of these withdrawals removes any human flexibility, transforming the banking application into an active source of stress.

- The Cycle of Emotional Exhaustion and Compensation: As chronic financial stress compromises an individual's psychological well-being, they frequently experience a distinct status deficit. To counteract the internal feelings of anxiety and entrapment, they often turn back to the market for short-term emotional relief. This manifests as a fresh round of impulse purchases financed through quick-access credit, creating a destructive feedback loop: borrowing to consume, experiencing burnout from the debt burden, and borrowing again to cope with the emotional exhaustion.

Macroeconomic Vulnerabilities: The Fragile Middle Class

When these micro-level behavioural patterns expand across millions of urban households, they coalesce into systemic macroeconomic vulnerabilities. India’s historical insulation against global economic shocks has long been credited to its remarkably high household savings rates, which provided a reliable source of internal capital. The rapid financialization of consumption poses a clear, long-term threat to this macroeconomic stabiliser.

The Depletion of Net Financial Savings

The structural shift in the household balance sheet is unmistakable. As gross debt continues to rise, the net financial savings of households have fallen to historic lows.

With net financial savings dropping to historic lows, the traditional domestic cushion against macro shocks is significantly thinner. Money that was once channelled into long-term capital formation instruments—such as public provident funds, fixed deposits, and life insurance policies—is now systematically consumed by short-term interest payments and e-commerce checkout settlements.

Systemic Risks Highlighted by the Regulator

The Reserve Bank of India (RBI) has repeatedly issued formal warnings regarding the unsustainable expansion of unsecured retail loans. In its comprehensive Financial Stability Reports, the central bank has pointed out several vulnerabilities that could threaten the broader financial ecosystem:

- The Rise of Delinquency in Small-Ticket Loans: The most severe increases in non-performing assets (NPAs) are concentrated within micro-loans below ₹50,000 (Mojon, 2023). These segments are heavily populated by young, first-time borrowers who lack deep financial literacy or stable income streams.

- The Hidden Risks of Cross-Leverage: Because digital lending applications operate outside the traditional, rigid framework of centralised banking credit checks, an individual can easily borrow from multiple distinct fintech platforms simultaneously (Mojon, 2023). This creates a hidden web of cross-leverage, where a borrower uses credit from one platform to service an overdue EMI on another, masking the true extent of systemic credit risk.

- The Threat of Unexpected Economic Friction: The systemic danger of a highly leveraged middle class is its complete vulnerability to macroeconomic shifts. If the economy faces unexpected global crosswinds, inflation shocks, or corporate restructurings, even a modest rise in unemployment or income stagnation would trigger a chain reaction of defaults across the consumer credit ecosystem. Because these loans are entirely unsecured, the financial institutions backing them would face rapid capital erosion, threatening stability across the wider banking system.

Reclaiming the Future: Strategies for Financial De-escalation

Reversing the momentum of the pay-later lifestyle requires a coordinated effort that spans regulatory oversight, corporate accountability, and a profound cultural reassessment of our relationship with money. India cannot afford to allow its demographic dividend to be hollowed out by a systemic crisis of consumer debt.

Institutional and Regulatory Reform

The Reserve Bank of India must continue to transition from a responsive regulator to a proactive architect of digital credit boundaries.

- Mandatory "Cooling-Off" Windows: Regulatory bodies should mandate a compulsory twelve-hour cooling-off window for all unsecured consumer durable loans above a specific value threshold. The instantaneous, one-click disbursal model must be intentionally slowed down to reintroduce healthy cognitive friction into the transaction process.

- Holistic Debt-to-Income Caps: Financial platforms must be legally required to evaluate a borrower’s total, cross-platform EMI obligations against verified tax records or bank statement inflows. Institutional credit should be restricted if an individual’s total monthly repayment commitments cross a hard ceiling of their documented net income.

- Plain-English Disclosure Architectures: The marketing of "No-Cost EMIs" must be replaced by absolute transparency. Platforms should be legally mandated to display the total absolute cost of an asset—including all backend merchant commissions, processing fees, and potential late-payment penalty rates—in bold, unmistakable terms at the final digital checkout screen.

Cultural and Individual Strategies

At the individual level, breaking free from gilded entrapment requires a conscious structural uncoupling from the values of performative consumption.

- Reclaiming Slow Consumption: Consumers must actively rebuild the psychological capacity for delayed gratification. Implementing self-imposed friction—such as forcing a thirty-day waiting window before purchasing any non-essential asset—can effectively neutralise algorithmic manipulation and emotional impulse buying.

- The Re-anchoring of Personal Status: The urban middle class must deliberately decouple personal worth from the display of depreciating consumer assets. True financial security—measured by the existence of emergency reserves, liquid investment portfolios, and career mobility—must be culturally elevated over the fragile projection of leveraged wealth.

- The Capital Cushion Strategy: Young professionals should commit to a structural financial rule: no consumer asset should be purchased via leverage unless the individual possesses twice its absolute value in liquid cash reserves. By treating credit strictly as an operational choice rather than a mechanism for synthetic affordability, the consumer can successfully reclaim control over their financial independence.

The Price of Peace

The transformation of India's financial landscape from a culture of patient saving to an environment of instant, leveraged gratification represents a defining sociological shift of our time. The Equated Monthly Instalment, which entered the market as a tool for economic access and upward mobility, has mutated into an instrument of emotional and psychological exhaustion.

The modern "Pay-Later Generation" stands at a historic crossroads. They enjoy access to an array of global luxuries, experiences, and technological marvels that their parents could scarcely imagine. Yet, the systemic financialization of their daily lives has exacted an incredibly steep tax. By outsourcing their future income to pay for immediate desires, millions of young Indians have entered a state of modern indentured security—trapped in stressful careers, burdened by chronic underlying anxiety, and constantly managing a precarious web of automated debt obligations.

Ultimately, this crisis is not an issue of currency; it is a profound conflict over identity, lifestyle stability, and our shared understanding of happiness. A society that evaluates its progress solely by the speed of its transactions and the visual polish of its consumption will eventually discover that its material wealth rests on a deeply fragile foundation. In an era obsessed with instant gratification, where every dream can be seamlessly split into twelve easy instalments, we must finally confront the underlying economic truth: when your future is fully leveraged, the one asset that can never be bought back is peace itself.

References

- Bian, W., Cong, L., & Ji, Y. (2023). The Rise of E-Wallets and Buy-Now-Pay-Later: Payment Competition, Credit Expansion, and Consumer Behaviour. SSRN Electronic Journal. https://doi.org

- Deepika, R., & Meena, S. (2025). Online consumer buying behaviours and the psychological detachment of cost in digital finance frameworks. Indian Journal of Marketing Research, 14(2), 45–58.

- deHaan, E. (2024). Buy Now Pay (Pain?) Later. Management Science, 70(3), 1420–1438.

- Kumar, A., Salo, J., & Bezawada, R. (2024). The effects of buy now, pay later (BNPL) on customers’ online purchase behaviour. Journal of Retailing, 100(4), 602–617. https://doi.org

- Menon, R. (2024). Is rising consumer credit a cause for concern? Journal of Banking and Financial Perspectives, 29(3), 112–118.

- Mojon, B. (2023). Buy now, pay later: a cross-country analysis. BIS Quarterly Review, December, 63–75.

- Nair, A. (2026). Study of Buy-Now-Pay-Later (BNPL) Adoption Among Students and Its Impact on Spending Patterns. Journal of Advanced Financial Research, 16(1), 12–29.

- Nitsure, R. R. (2026). Macroeconomic Perspectives and the Financialization of Household Balance Sheets. Symbiosis School of Economics Macro Report, January 4–9.